On the 28th of September 2024, many a Zimbabwean became aware of the resolutions of the monetary policy committee meeting held the day before. A number of resolutions were made which included an increase in the bank policy rate from 20% to 35% and reduction of the amount of forex an individual can take out of the country from US$10,000 to US$2,000.

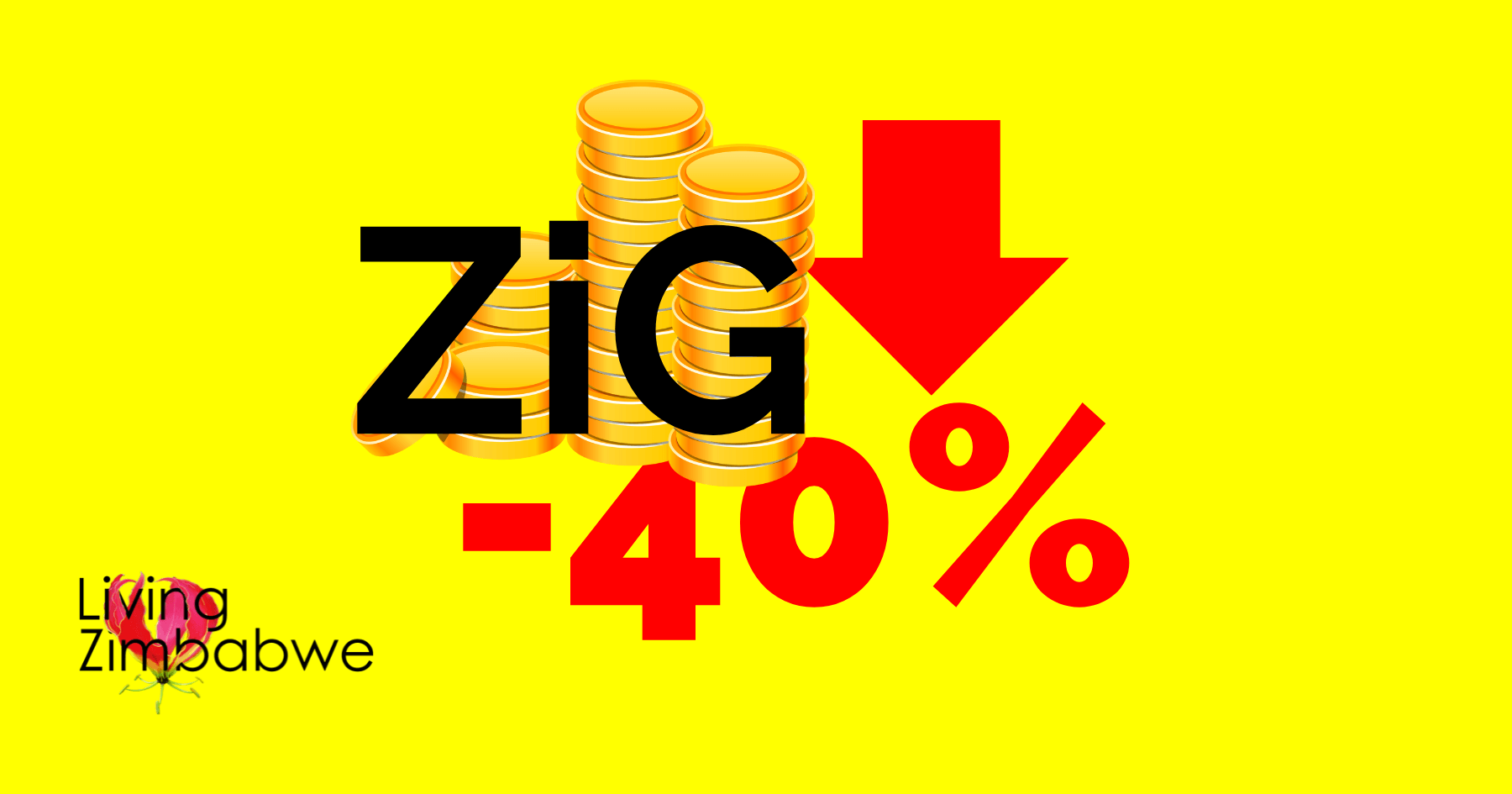

For people on the ground, the most significant impact was the devaluation of the ZiG from US$1:13.5 to US$1:25. This move knocked just over 40% off the value of the ZiG (The Zimbabwe Gold (ZiG; code: ZWG) just under six months after its introduction as official currency in April 2024). So, from one day to the next, your money was worth a lot less than what it was (again!).

Is the ZiG a Reliable Store of Value?

This begs the question, what’s the point of transacting in or holding the ZiG if it can be drastically devalued just like that? Many traders no longer (some haven’t for a while) accept ZiG and prefer to transact in the ‘stable’ US dollars.

The US dollar has for the ages been the world’s reserve currency but who knows how long that will hold with BRICS nations looking to establish a new currency? Where would that leave us USD addicted Zimbabweans? How would we trade and save?

Protecting Wealth in an Unstable Environment

The daily grind is not just about survival, it’s also about thriving and getting ahead financially. This is easier said than done especially in economies where decisions can take you backwards or almost wipe out possibly years of savings at no fault of your own. How do you build and protect your wealth?

Should Zimbabweans completely turn their backs on the ZiG and look to alternatives like the US dollar, physical gold, or cryptocurrencies like Bitcoin or stablecoins? These asset classes offer varying degrees of stability and growth potential, but each comes with its own risks. Read: Is it time for Zimbabwe to adopt Bitcoin, stablecoins and other cryptocurrency?

Gold, for example, is a traditional store of value, especially in uncertain times. Cryptocurrencies like Bitcoin which are volatile are gaining attention for amongst other things being a hedge against inflation and government interference. Stablecoins, which are pegged to assets like the US dollar have the same advantages as crypto without the extreme price swings.

Key Insights:

- ZiG to USD: ZiG has devalued by 40% since its introduction in April 2024.

- Zimbabwe Gold Price (per gram): Local gold prices increased by over 20% between April and September 2024.

- World Gold Price (per ounce): Global gold prices have risen by 17.2% from April to September 2024.

- Bitcoin: Bitcoin showed a slight decline (-3.23%) from April to September 2024 but had a substantial gain (+138.74%) from September 2023 to September 2024.

Planning for the Future

Time waits for no one and as it ticks along, we age. As we age, financial security becomes even more important, particularly with the potential for increased medical costs and reduced income in later years. Decisions made today about how to protect and grow wealth will have lasting consequences for the future.

Not only should the short-term impact of currency devaluation be considered, but also a long-term strategy for wealth preservation. Is it better to move completely to US dollars? Is cryptocurrency the way to go? Or is it best to stick with the primary store of value, gold?

What are you doing to protect your wealth and financial future in this unpredictable environment?

Disclaimer: The content provided is for informational purposes only and should not be considered financial advice. These are ideas and suggestions for potential ways to preserve and grow wealth in the Zimbabwean context. Always consult with a qualified financial advisor before making any financial decisions.